Borrowing Base

“No Smoke. No Mirrors…Only the Collateral That Counts”

A Borrowing Base is a mechanism that determines the amount of money a lender is willing to lend a business, based on the value of its eligible assets — typically accounts receivable, inventory, equipment, and sometimes real estate.

It’s a dynamic limit, recalculated regularly, and it determines the maximum availability under a revolving line of credit or asset‑based lending (ABL) facility.

Think of the borrowing base as a “collateral‑derived credit ceiling” – not a fixed number, but a fluctuating value tied directly to a company’s (fluctuating) asset performance.

Put another way, the borrowing base acts as the upper limit of funds that can be drawn.

As the value of the collateral changes, the borrowing base (and funds availability) changes accordingly.

Key Characteristics

- Dynamic: Rises and falls with your eligible assets.

- Collateral‑Driven: Calculated strictly on asset value and advance rates.

- Lender Defined: Advance rates and eligibility rules are set forth in the credit agreement.

- Risk‑Managed: Lenders use reserves and eligibility criteria to protect value.

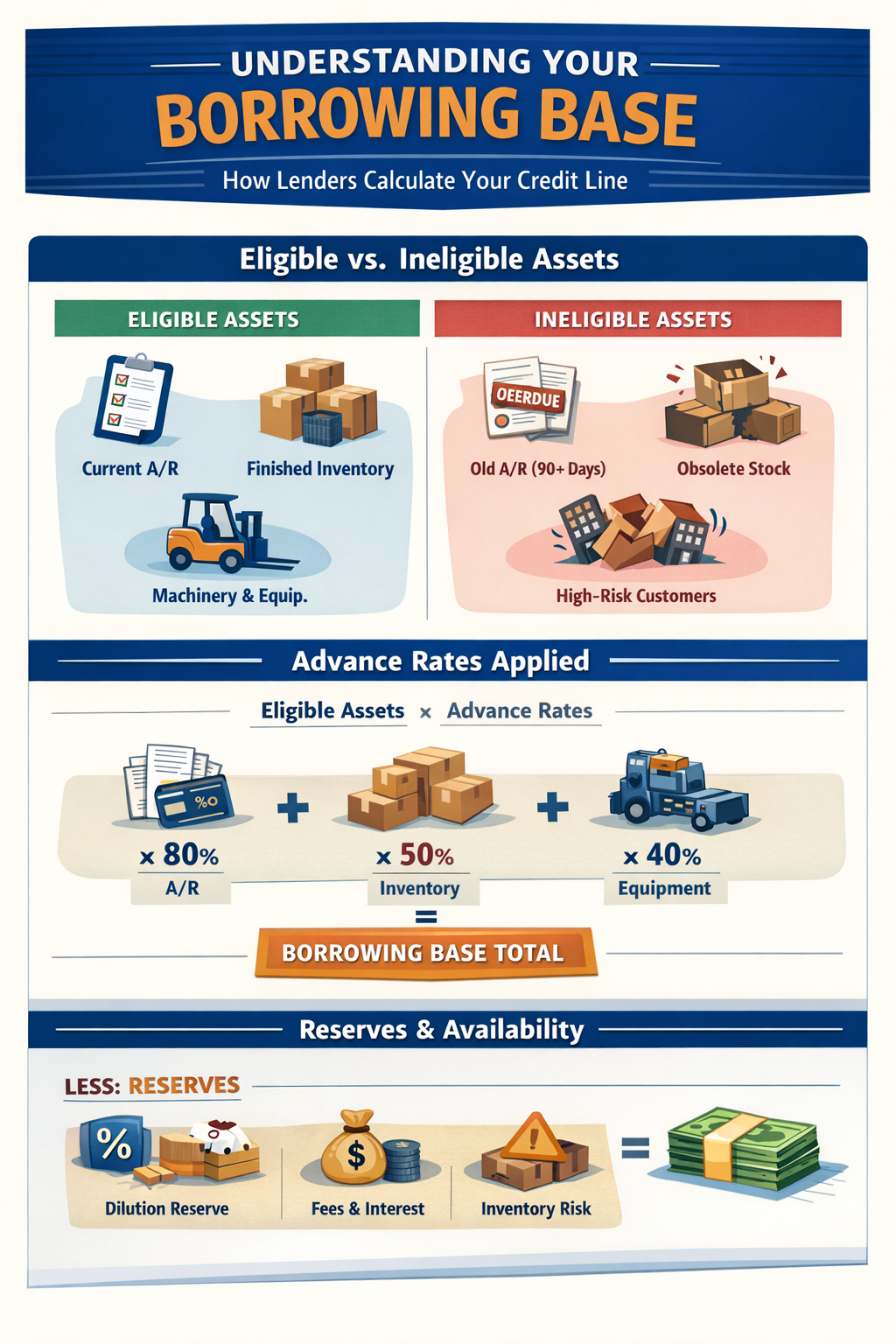

🔷 Included Assets🔷

Borrowing base assets vary by lender, but the most common include:

✦ Accounts Receivable (AR)

- Eligible AR: typically invoices under a certain age (e.g., <90 days).

- Ineligible items often include past‑due, disputed, or bankrupt customer balances.

✦ Inventory

- Finished goods and raw materials (valued at lower advance rates).

- Requires inventory reporting and sometimes physical counts.

✦ Other Collateral (Less Common)

- Equipment or machinery (with appraised value).

- Commercial real estate (in certain structures)

🔷 Advance Rates & Eligibility🔷

| Asset Type | Common Advance Range |

|---|---|

| Accounts Receivable | ~70%–90% |

| Inventory | ~25%–60% |

| Equipment | Varies |

| Commercial RE | Depends on LTV |

Advance rates reflect how easily the asset can be converted to cash, risk of loss, and historical performance.

⚙ How the Borrowing Base Is Calculated

Lenders assign an advance rate to eligible assets — a percentage of the collateral value they are willing to finance.

The borrowing base is the sum of each eligible asset (less ineligible amounts) multiplied by its advance rate.

📐 Basic Formula:

(Accounts Receivable – Ineligible Amount × AR Advance Rate)

+ (Inventory – Ineligible Amount × INV Advance Rate)

+ (any other included assets)

− Reserves*

= Borrowing Base

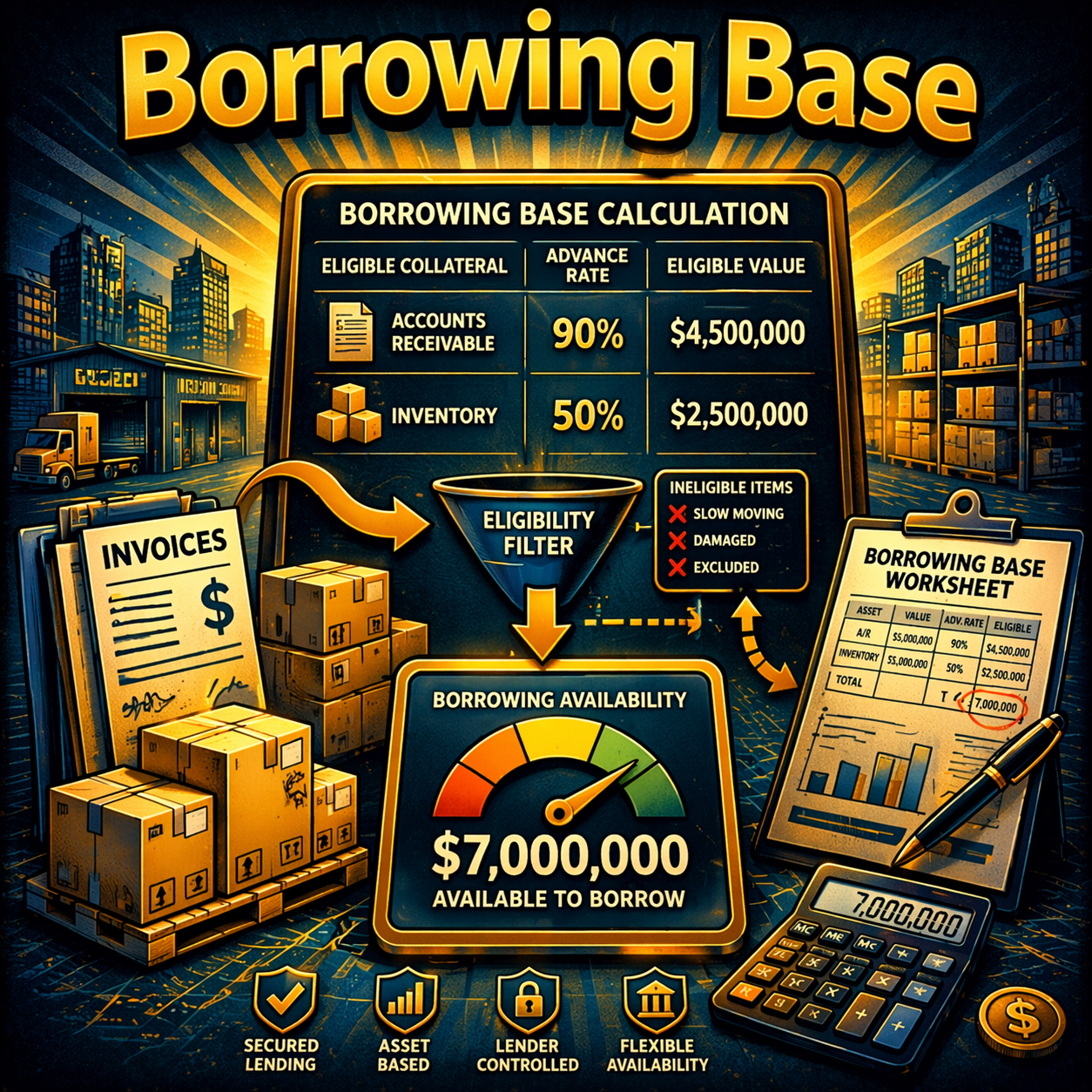

Basic Example: Borrowing Base Calculation Snapshot

| Asset Class | Gross Value | Ineligible Amount | Eligible Amount | Advance Rate | Borrowing Base Value |

|---|---|---|---|---|---|

| Accounts Receivable | $1,200,000 | $200,000 (90+ days past due) | $1,000,000 | 80% | $800,000 |

| Inventory (Finished) | $900,000 | $100,000 (obsolete/unsellable) | $800,000 | 50% | $400,000 |

| Subtotal | $1,200,000 | ||||

| Less: Reserves | – $100,000 (fees, dilution, etc.) | ||||

| Net Loan Availability | $1,100,000 |

What This Shows:

Even though the company has $2.1M in gross collateral, only $1.8M is eligible, and after applying advance rates and reserves, the actual amount available to borrow is $1.1M.

*Common Reserves & Deductions

Lenders typically deduct reserves from the borrowing base to protect their exposure, such as:

- Dilution Reserves (returns, credits, bad debts).

- Fees & Interest Reserves (audit, field exam costs).

- Inventory Risk Reserves (older or slow‑moving stock).

📑 Borrowing Base Certificates (BBC)

A Borrowing Base Certificate is the formal report a borrower submits to the lender at regular intervals (monthly, weekly, etc.) detailing:

List of eligible AR and inventory

Aging reports

Ineligible assets or deductions

Calculated borrowing base

Lenders use this certificate to recalculate availability and ensure the loan stays within agreed limits.

🌀 Borrowing Base vs. Credit Limit

A credit agreement might specify a total credit limit (e.g., $2M), but the borrowing base is the active limit based on current collateral. A borrower can only draw against what the borrowing base supports, not simply the maximum credit line.

⦿ The Impact of Borrowing Bases

🎯 1. Loan Capacity

The borrowing base directly determines how much a business can borrow at any point — no matter what its total approved credit line is in the credit agreement.

📈 2. Dynamic Liquidity

As AR increases or inventory turns over, the borrowing base can rise — providing access to more working capital when needed.

⚠️ 3. Risk Management

Lenders manage risk through eligibility criteria, reserves, and advance rates to protect against collateral value decline.

📊 4. Operational Discipline

Accurate reporting and internal controls are essential since misreporting can trigger deficiencies or require cash injections to correct a deficit.

⚙ Borrowing Base: Expanded Example Calculation

Scenario:

Midline Manufacturing Co. is applying for a $3,000,000 asset-based line of credit. The lender agrees to base availability on accounts receivable, finished goods inventory, and equipment. Advance rates and eligibility criteria are outlined in the credit agreement.

Here’s how the borrowing base is calculated:

🔸 Step 1: Eligible Collateral Summary

Asset Type | Gross Value | Ineligible | Eligible Amount | Advance Rate | Borrowing Base Value |

Accounts Receivable | $1,400,000 | $250,000 (over 90 days) | $1,150,000 | 80% | $920,000 |

Inventory (Finished) | $1,000,000 | $150,000 (obsolete/slow) | $850,000 | 50% | $425,000 |

Equipment | $900,000 (appraised) | N/A | $900,000 | 40% | $360,000 |

🔸 Step 2: Borrowing Base Total

- $920,000 (AR)

- $425,000 (Inventory)

- $360,000 (Equipment)

= $1,705,000

🔸 Step 3: Reserves and Net Availability

Component | Amount |

Borrowing Base Total | $1,705,000 |

Less: Lender Reserve | – $105,000 (for dilution, fees, and margin) |

Net Loan Availability | $1,600,000 |

🔸 Notes:

- Advance rates are based on historical asset performance and lender risk appetite.

- Reserves protect the lender against payment delays, disputes, or other operational risks.

- The borrowing base is recalculated monthly using updated AR aging and inventory reports.

- Loan draws are limited to the lesser of the borrowing base or the credit facility cap.

What This Demonstrates:

This example illustrates how a business with over $3 million in gross assets can unlock $1.6 million in liquidity — using the value of its existing, verified collateral. The borrowing base ensures the lender’s exposure is aligned with real-time asset value, while giving the borrower flexible working capital access.

Best Practices for Managing a Borrowing Base

✅ Keep AR aging tight and disputes resolved quickly

✅ Conduct regular inventory reviews

✅ Maintain clean documentation and reconciliation processes

✅ Understand lender advance rates and ineligibles

✅ Plan for seasonal swings in accounts receivable and inventory

🧠 Final Thought

The borrowing base is more than a calculation — it’s a living measure of how a business’s assets translate into real borrowing capacity. For businesses using asset‑based financing, mastering borrowing base mechanics is essential to maintaining liquidity, managing risk, and negotiating better credit terms.