Defeasance

“Swap the prop, keep the drop!”

(Swap out the property, keep those loan payments flowing.)

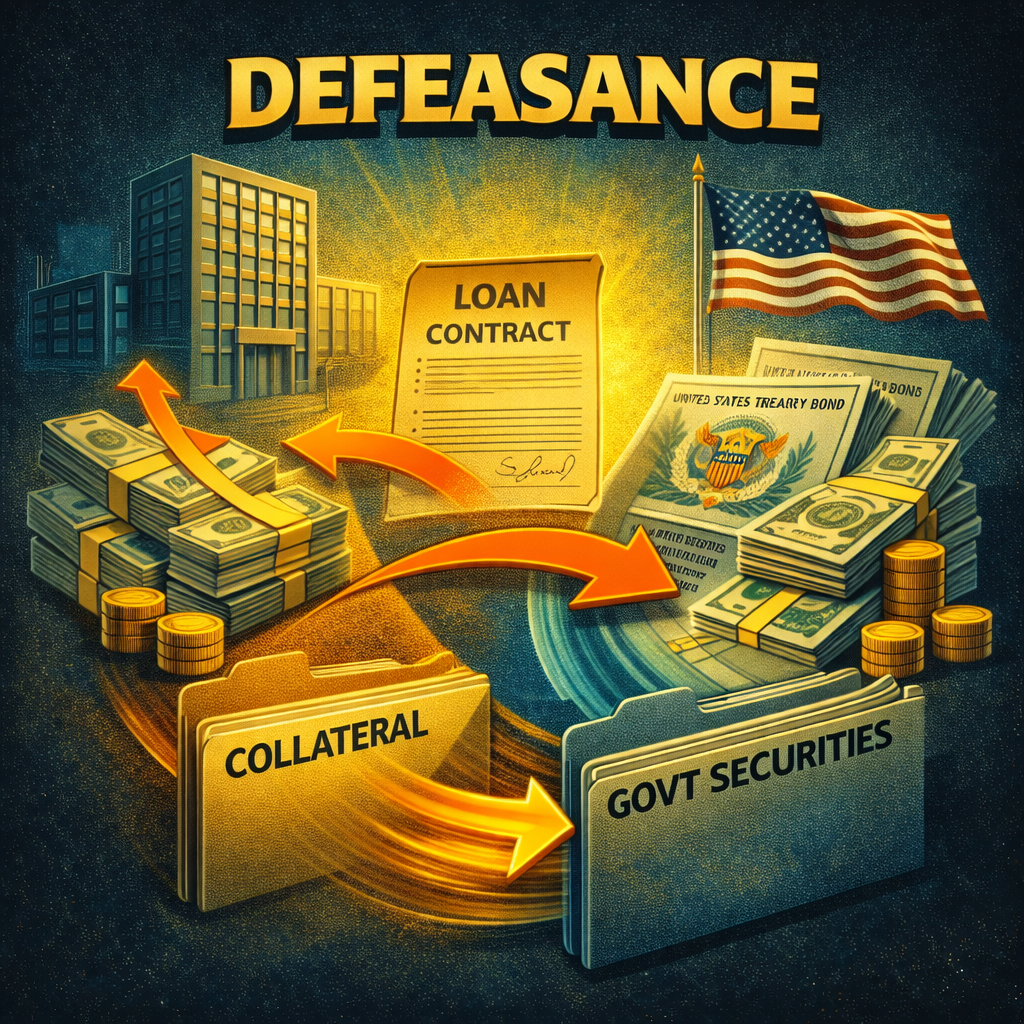

Defeasance is a prepayment method used in commercial real estate loans where, instead of paying off the loan directly, the borrower replaces the collateral with government securities. These securities generate cash flows that match the loan’s remaining payments, ensuring the lender receives the full scheduled interest and principal. Defeasance allows property owners to release the property from the loan lien, often to facilitate a sale or refinancing without triggering penalties.

Discussion

Defeasance is fairly common in the commercial real estate loan market, particularly for securitized loans such as those included in Commercial Mortgage-Backed Securities (CMBS).

Here’s a breakdown of its prevalence:

- CMBS Loans: Defeasance is standard and widely used because these loans are structured for investors expecting fixed cash flows. Prepaying a CMBS loan directly would disrupt those payments, so defeasance offers a compliant workaround.

- Life Company Loans and Other Fixed-Rate Loans: Defeasance is less common but still used, depending on the lender’s requirements and whether yield maintenance or step-down penalties are specified instead.

- Multifamily, Retail, and Office Sectors: It’s especially common in income-producing properties that are refinanced or sold before loan maturity.

In summary, defeasance is a standard prepayment mechanism in structured finance and is commonly required in CMBS lending, making it a well-known but somewhat specialized option outside that context.

Defeasance Example:

A real estate investor owns a shopping center financed with a $5 million CMBS loan at a fixed 5% interest rate with 8 years remaining. The investor wants to sell the property now, but the loan terms do not allow traditional prepayment due to strict CMBS restrictions.

Solution: Defeasance

Instead of repaying the loan, the borrower works with a defeasance consultant to purchase a portfolio of U.S. Treasury securities. These securities are structured to generate exactly the same cash flows—in both timing and amount—as the remaining loan payments.

- The collateral for the loan is substituted: the Treasury portfolio replaces the shopping center as security.

- The loan remains in place and continues to pay scheduled interest and principal from the Treasury cash flows.

- The borrower is released from the loan and can sell the property free of the lien.

Outcome:

- The buyer gets the property without the loan attached.

- The lender continues to receive uninterrupted payments.

- The seller pays transaction costs and possibly a premium for the securities, but avoids yield maintenance penalties or the inability to sell.

Defeasance allows flexibility while preserving the financial integrity of the securitized loan.