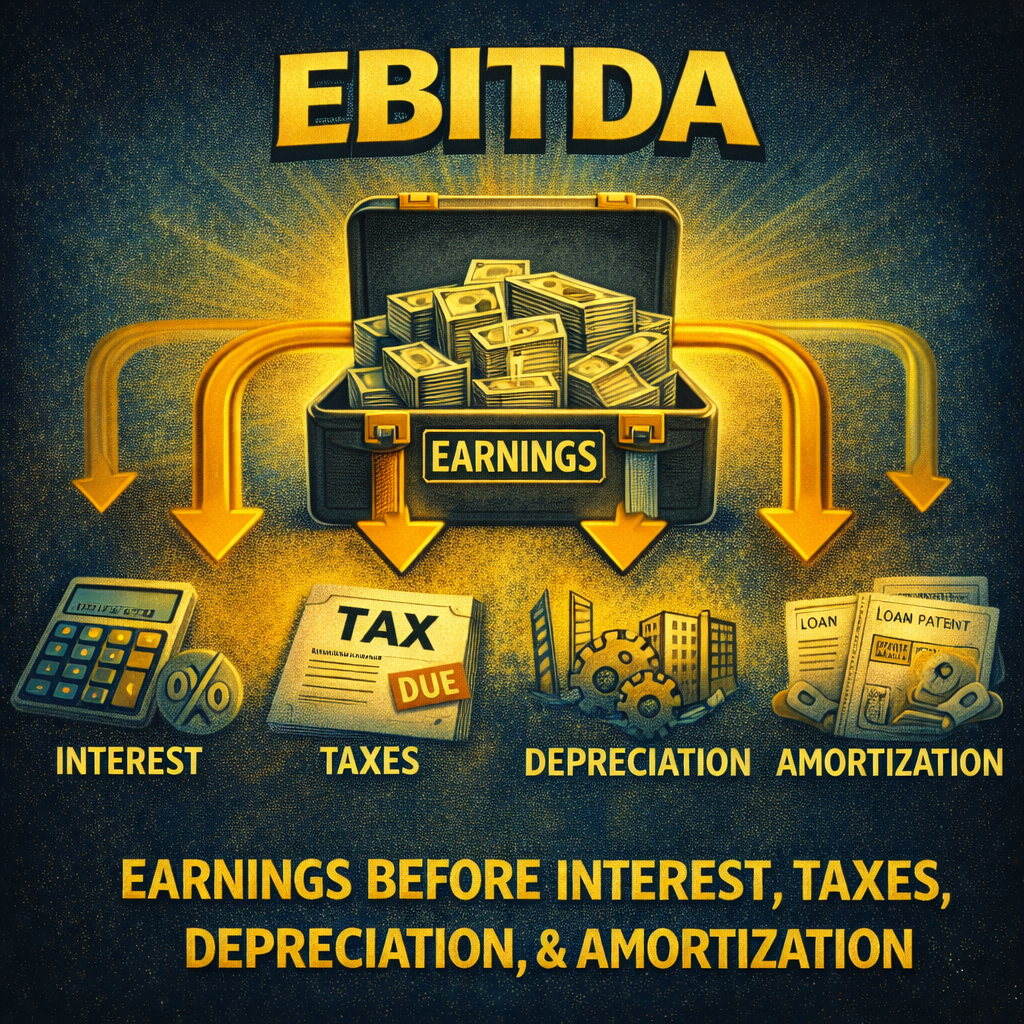

EBITDA

“EBITDA: Show Me the Real Money”

(sort of)

EBITDA stands for: Earnings Before Interest, Taxes, Depreciation, and Amortization.

It is a financial metric used to assess a company’s operating performance and profitability before the impact of financial structure, tax environment, and accounting decisions. By excluding non-operational expenses, EBITDA provides a clear view of core profitability and cash flow potential.

By focusing purely on operating results, EBITDA helps stakeholders understand how well a business is performing from its core operations, without distractions from financing or accounting complexities.

Components of EBITDA

EBITDA starts with net income, and adds back the following:

- Interest: Costs associated with debt financing. Excluding this shows earnings independent of capital structure.

- Taxes: These can vary by region and strategy; removing them helps standardize performance.

- Depreciation: A non-cash expense related to tangible assets (like machinery and equipment).

- Amortization: A non-cash expense related to intangible assets (like patents or goodwill).

Why EBITDA Is Useful – Strengths of EBITDA

Focuses on Core Operations

It strips out interest, taxes, depreciation, and amortization—so you see how the actual business performs, regardless of capital structure or tax environment.

Useful for Comparisons

Makes it easier to compare companies across industries or regions, especially those with different levels of debt or asset ownership.

Cash Flow Proxy

Since it removes non-cash expenses, EBITDA gives a rough idea of how much cash a company generates from operations.

Valuation Tool

Often used in enterprise value multiples (e.g., EV/EBITDA) for valuing businesses, especially in private equity and M&A deals.

Removes Accounting Variability

Helps normalize performance across companies with different accounting methods for depreciation/amortization.

EBITDA, in plain language . . .

. . . is a way to look at how much money a business really makes from its day-to-day work,

without getting distracted by loans, taxes, or accounting tricks.

When to Use EBITDA

Lender Assessments:

Measuring Debt Service Capacity

Banks and lenders want to know if a company can handle its debt payments. Since EBITDA strips out interest and taxes, it reflects how much raw cash is available to meet obligations.

Internal Performance Analysis:

Operating Strength of Units

Large companies or conglomerates often manage multiple business units. EBITDA helps compare them without distortions caused by how assets are financed (debt vs. equity), local tax rates, and varying depreciation schedules.

Private Equity & M&A:

Evaluating Acquisition Targets

In mergers & acquisitions (M&A), EBITDA is a quick and standardized way to compare potential targets. Buyers want to know how much the business earns from its core operations, before interest, taxes, and non-cash items like depreciation.

EBITDA Limitations

“EBITDA: The Makeup, Not the Face”

Where EBITDA falls short – Weaknesses of EBITDA

Ignores Real Costs

Depreciation and amortization reflect real wear and tear or intangible value loss. Ignoring them can make a business look healthier than it is.

Not a Cash Flow Measure

While it’s close, EBITDA isn’t true cash flow. It ignores capital expenditures, working capital changes, and debt repayments.

Can Hide Financial Risk

By excluding interest and taxes, EBITDA may mask issues like high debt levels or tax burdens that affect long-term viability.

Not GAAP-Standardized

EBITDA isn’t defined by GAAP (Generally Accepted Accounting Principals), so companies can calculate it differently. This can lead to inconsistent or manipulated results.

Can Be Misused

Sometimes used to “dress up” poor financials. Just because EBITDA looks strong doesn’t mean the business is sustainable.

Real-World Analogy: Food Truck

Imagine a food truck that pulls in $20,000 a month in sales.

If you want to know how well the operation is doing before thinking about the truck loan, taxes, or the condition of the truck, you’re talking EBITDA.

But if the truck is falling apart and they owe money on the truck itself along with another loan for the equipment inside the truck, plus taxes in arrears?

EBITDA won’t show that.

Real-World Analogy: The Gym

Imagine a gym that earns $50,000/mo. from memberships.

If you just look at how much money it’s pulling in before paying interest on its loans, taxes, or accounting for wear and tear on equipment, you’re looking at EBITDA.

On paper, the gym looks strong—steady cash & signups.

But behind the scenes:

- The treadmills are breaking down

- Lease payments are stacking up

- The gym owes big money on a recent expansion loan

EBITDA won’t show any of that.

EBITDA - The Practical Side of Things

Good for comparisons:

It helps compare different companies more fairly—even if one owns all of their equipment and the other rents theirs.

Cleaner picture:

It shows how profitable the actual business engine is, before other stuff messes with the numbers.

But be careful:

It can look better than reality—because it ignores real costs like aging equipment, debt, and taxes that eventually

have to be paid.

BOTTOM LINE

EBITDA is a useful lens—but it’s not x-ray vision – it’s not the whole story.

Use it smartly, double-check the math, and never stop at the surface. Use it with eyes open.