Loan Structuring

In Commercial Finance

“Frame It Tight, Fund It Right.”

Loan Structuring in Commercial Lending refers to the process of designing a loan in a way that meets the borrower’s financial needs while minimizing risk for the lender. It’s one of the most critical aspects of commercial banking and business finance, requiring a deep understanding of both the borrower’s business model and the lender’s risk tolerance.

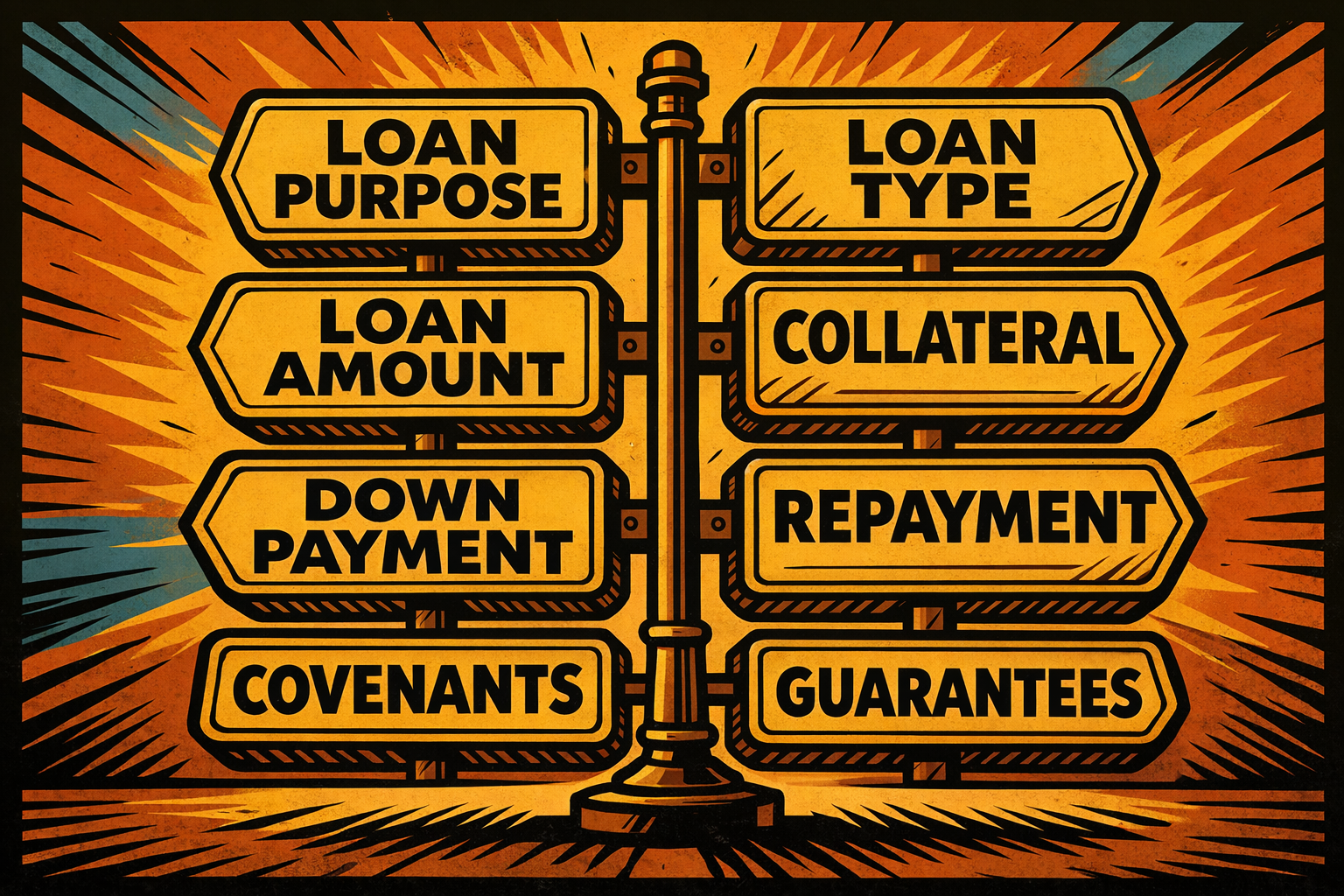

Core Elements

of Loan Structuring

Loan Purpose

Understanding the why behind the loan is foundational. Examples include:

Acquisition: Buying a business, property, or major asset like equipment. These loans are usually long-term and secured.

Working Capital: Used for operational expenses like payroll, inventory, or seasonal cash flow gaps.

Expansion: To fund growth initiatives—such as opening a new location, launching a product, or entering a new market.

Refinancing: Paying off existing debt with more favorable terms (lower rate, longer term, improved cash flow).

Each purpose comes with a different risk profile, which affects how the loan is structured.

Loan Type

Choosing the right loan vehicle is essential to matching cash flow and repayment capability. Examples include:

Term Loan: A lump sum repaid in installments. Often used for long-term assets or business acquisitions.

Revolving Line of Credit (LOC): Businesses borrow what they need, repay/pay-down, and reuse (up the the LOC amount limit). Ideal for cash flow variability.

Bridge Loan: A short-term, often interest-only loan designed to “bridge the gap” between a current need for funding and the future availability of longer-term or permanent financing.

Construction Loan: Disbursed in draws based on project progress. Typically converts into a term loan after completion.

Loan Amount

The dollar amount a borrower qualifies for depends on:

Cash Flow: Typically measured by the Debt Service Coverage Ratio (DSCR). Most lenders require a DSCR of 1.20 or higher.

Collateral Value: Affects how much a bank is willing to lend (Loan-to-Value ratio or LTV).

Purpose Fit: The loan amount must align with the capital need — not more, not less.

Lenders also look at historical performance and projections to size the loan appropriately.

Collateral

The asset pledged to secure the loan, which the lender can seize if the borrower defaults.

Hard Assets: Real estate, equipment, vehicles.

Liquid Assets: Cash, marketable securities.

Receivables/Inventory: Used for lines of credit, but often discounted based on collectability.

Blanket Liens: A claim on all business assets.

Lenders assess collateral quality, marketability, and depreciation risk.

Repayment Structure

Repayment methodologies affect both lender risk and borrower cash flow.

- Term: The actual loan duration, before maturity or refinancing.

Amortization Period: The time it would take to fully repay the loan. Often longer than the actual loan term (e.g., 5-year loan with 15- or 20-year amortization).

Balloon Payments: Many commercial loans require a large payment at the end of term if not fully amortized.

Interest Rate: Can be fixed (predictable) or floating (adjusts with market rates, e.g., SOFR or Prime + margin).

Payment Frequency: Monthly is standard, but quarterly or seasonal structures may be used based on business needs.

Covenants

Loan covenants are conditions written into the loan agreement to manage lender risk.

Financial Covenants: Metrics the borrower must maintain, such as:

DSCR (e.g., must stay above 1.25)

Leverage Ratio (Debt/EBITDA limits)

Minimum Net Worth or liquidity

Affirmative Covenants: Actions the borrower must take (e.g., provide financials quarterly, keep insurance active).

Negative Covenants: Things the borrower cannot do without approval (e.g., take on new debt, pay dividends, or sell assets).

Violating a covenant can trigger a loan default

even if payments are current.

Down Payment

The down payment is the borrower’s equity contribution toward the total cost of the asset or project being financed. It is a critical component of business finance because:

- Risk Mitigation: Reduces loan-to-value (LTV); less risk for lender.

- Creditworthiness Signal: Shows borrower has “skin in the game”. May result in better terms or approval.

- Improved DSCR: Smaller loan = lower debt service. Easier to meet covenant requirements

- Recourse Management: Higher equity may reduce need for full recourse. Can limit exposure to personal guarantees.

Guarantees

Lenders often require guarantees to add a layer of protection.

Personal Guarantees: Business owners personally back the loan, meaning their personal assets are at risk.

Corporate Guarantees: A parent or affiliate company guarantees repayment.

Limited Guarantees: May be capped by time or dollar amount, especially in partnerships.

Guarantees signal confidence in the deal—and give lenders more legal recourse.

Loan Structuring Scenarios

| Scenario | Loan Type | Term | Amortization | Collateral | Covenants | Exit Strategy | Guarantees |

| Equipment Financing | Term Loan | 3 to 7 years | Straight-line or accelerated | Equipment financed | Loan-to-value cap, DSCR min | Repayment through cash-flow or asset sale | Personal guarantees from business owners typically required |

| Accounts Receivable Financing | Revolving Line of Credit | 1-year revolving (renewable) | None (interest only) | Eligible accounts receivable | A/R aging limits, possibly Borrowing Base | Repaid as receivables convert to cash | Typically require PG if borrower is closely held or credit is weak |

| Construction-to-Perm Financing (Owner-Occupied) | Construction-to-Perm Loan | 12-month construction + 25-year perm | Interest-only, then 25-year amortization | Property under construction | Construction progress, interest reserve | Refinanced into long-term mortgage | Often includes PGs during construction, may be released after stabilization |

| Fleet Expansion | Term Loans or Equipment Leases | 5 years | 60 months per vehicle | Fleet vehicles | Asset maintenance, Insurance, fleet limits | Repayment through cash flow or trade-in | Personal or corporate guarantees depending on entity structure |

| Refinancing Existing Debt | Senior Term Loan | 5 to 10 years | Extended to improve DSCR | Business assets and refinanced collateral | Refinance use oversight, leverage limits | Cash-flow from reduced interest burden, better terms | Personal guarantees often required, may be waived if loan is well-collateralized |

| Agricultural Operating Loan | Revolving Line of Credit | 12 months (seasonal) | None (interest only) | Crops, inventory | Crop sale timing, usage tracking | Crop sales repay balance | Often secured by crop insurance or USDA-backed, with PGs |

| Owner-Occupied Commercial Real Estate | Term Loan | 10 years | 25 years | Commercial real estate | DSCR, occupancy ratio | Cash-flow or Sale or refinance at term | PGs common unless property is held by established entity |

| Distressed Business (Turnaround Financing) | Bridge Loan | 12 to 18 months | None (balloon at maturity) | Business assets, possibly real estate | Likely several, closely monitored | Ideally cash-flow; sale of assets or long-term refinancing | Strong guarantees expected due to high-risk profile |

Key Considerations for Borrowers

Affordability

Structure should match cash flow cycles and avoid over-leverage.

Flexibility

Covenants and terms should not constrain operations unnecessarily.

Strategic Fit

Financing should align with business growth plans and capital structure.

Visibility & Certainty

Understand the terms clearly — amortization, balloon payments, rate adjustments, and fees.

Predictability in repayment helps with financial planning, especially in volatile industries.

Covenant Sensitivity

Some covenants may seem benign but can trigger technical defaults if not monitored.

Borrowers should request grace periods or cure rights if ratios are breached.

Prepayment Flexibility

Look for prepayment penalties or yield maintenance clauses that can limit refinancing options.

Some loans offer partial or full prepayment without penalty — a valuable feature if rates fall.

Loan Lifecycle & Exit Strategy

Understand what happens at maturity: refinance? balloon payment? sale of an asset?

For project-based or development loans, a clear exit is essential.

Documentation Burden

Ongoing requirements (monthly/quarterly financials, compliance certificates) can be time-consuming.

Seek to streamline reporting when possible — especially for small or growing companies.

Relationship Considerations

Is the lender likely to support future credit needs?

Strong relationships can yield better terms, flexibility in workouts, and faster approvals.

Total Cost of Capital

Look beyond the interest rate:

Origination fees

Legal and appraisal fees

Draw fees (for lines or construction)

Covenant compliance costs

Collateral Exposure

Be aware of how much of your business or personal assets are pledged.

Try to avoid cross-collateralization that limits borrowing flexibility in the future.

Key Considerations for Lenders

The fundamental pillars that guide how lenders and credit officers approach risk and return (the short form):

Risk Mitigation: Loan terms, covenants, and collateral are structured to protect the bank/lender.

Industry & Business Analysis: Understanding borrower cash flow and risk specific to their sector.

Regulatory Compliance: Loan must meet internal credit policies and external regulations

(e.g., ECOA, CRA, and FDIC guidance).Exit Strategy: Lenders must consider how the loan will be repaid, especially for short-term or high-risk loans.